You must have heard of this term a lot especially off late. ‘FACTOR INVESTING. Today’s blog will try and delve deeper into it.

We got interested in this concept long before it became a buzzword in India. We interviewed the pioneers of this domain in our STOIC INVESTING PODCAST series. Mebane Faber, Wesley Gray and Gary Antonacci laid bare the entire methodology, historic 100-year back-tests, and practical difficulties associated with its implementation.

This has become a buzzword off-late primarily due to SPIVA reports exposing the inability of large-cap mutual funds to beat their benchmark NIFTY. We saw 02 mutual funds launch a fund tracking the Nifty 200 Momentum 30 index. They are finally entering the domain we have been ruling since long.

So What is FACTOR Investing?

So, the starting hypothesis is that markets are efficient and therefore you should simply buy the Index (the whole market) itself. Your money will grow as the country grows. Individual brilliance if at all it exists after transaction and management fees is due to sheer randomness and is visible only post-facto. (No way to find which 01 of the 100 mutual funds will do well next year)

FACTOR is an anomaly to this general efficient market Rule. Factor or STYLE is a set of investing principles that generate above-market returns after accounting for transaction charges, management fees, and all other costs.

Historically, it has been empirically proved that the following STYLES (FACTORS) have generated outsized returns which cannot be attributed to randomness.

- VALUE INVESTING: Revert to the mean in Cheap companies.

- MOMENTUM INVESTING. What goes up, continues to go up before reverting to mean kicks in.

- EARNINGS INVESTING: Markets reward earnings growth.

- LOW VOLATILITY: low beta outperform the high beta

- QUALITY INVESTING: High ROCE, ROE businesses command a premium and do well.

If you wish to dig deeper into the workings of FACTOR portfolios in India, spend some time in reading this white paper written by Anish Teli

Long’ Factors, not ‘Short’ Change : Long Only Factor Portfolios in India

At MysticWealth we practice 02 of the above factors. We are operational since 2011 and have carved a niche for ourselves in these domains.

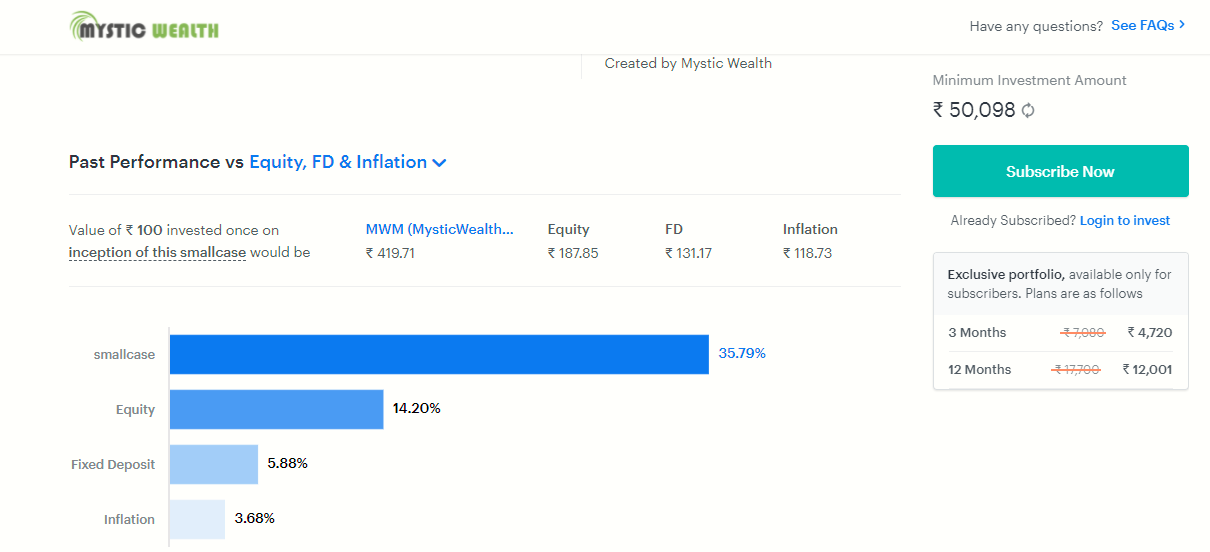

MWM: (MysticWealth Momentum)

is a 20 stock portfolio selected by a propitiatory algorithm ranking the stocks on the price momentum.

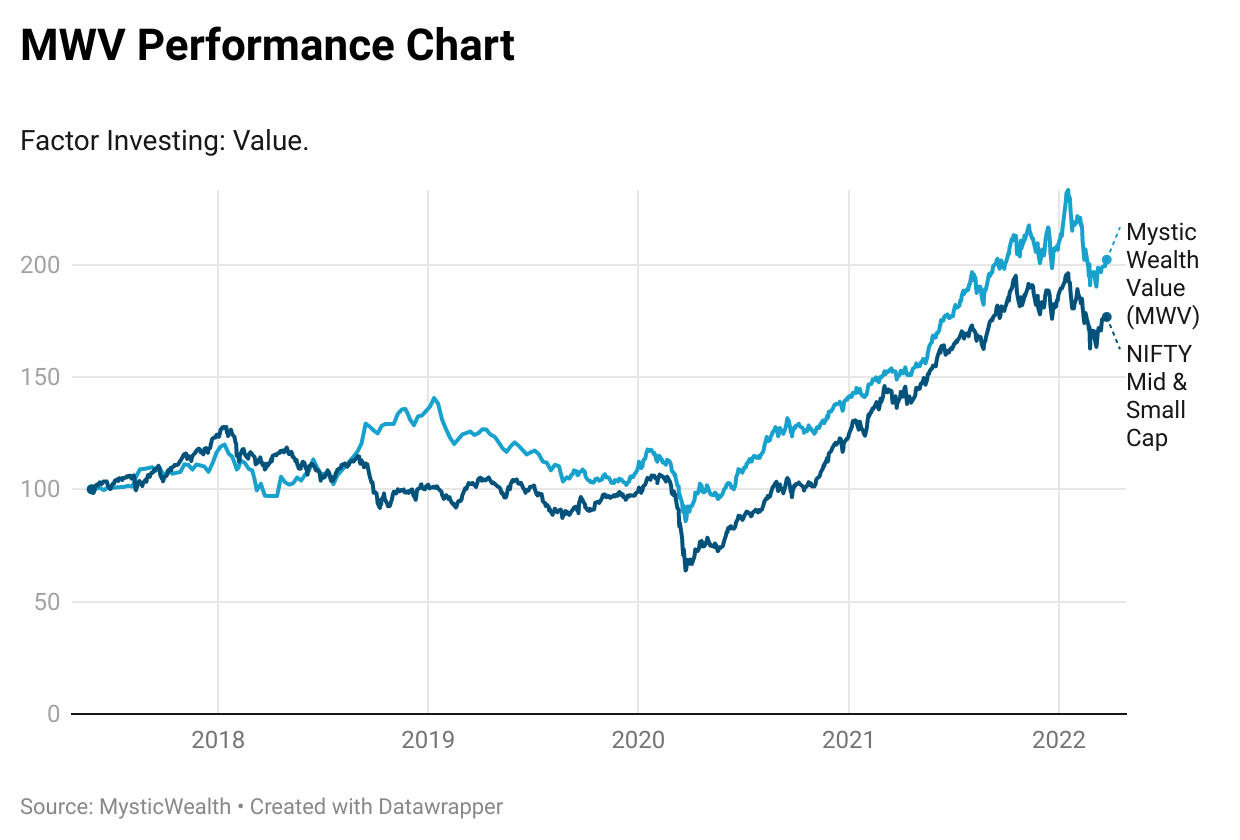

MWV: (MysticWealth Value)

sniffs for inefficiencies arising out of Spin-offs, demergers and other Special Situations. It also invests in GARP (Growth at reasonable Price) framework.

Both our FACTOR-based Model portfolios have beaten their benchmarks by a HUGE margin. While Momentum is in flavor now (2017-2022), Value generated big alpha in 2011-2014.